The world appreciates American farmers. They not only feed the planet, but they sow the seeds for the rest of the industry, which includes animal feed providers, technology and chemical innovators, processors, distributors and ultimately retailers.

Source: By Cheryl Meyer in Mergers & Acquisitions

“As the population continues to grow, and as diets get more sophisticated and consumers consume more protein, there’s going to be a need for more yield and more products,” predicts John Mickelson, managing partner of Midwest Growth Partners, a West Des Moines, Iowa-based private equity firm focused on underserved rural markets. MGP currently owns 20 food and ag-related platform companies in its portfolio, including Jackrabbit Equipment, a California maker of nut harvesting gear, such as carts and elevators.

But while many ag investors forecast sunny days ahead, the reality is that this is a tough industry to pursue. Outside growers can have shallow pockets and often depend on good weather and the U.S. government to turn a profit. If growers fail, that slump trickles to the rest of the trade. “The returns have not materialized in the last 12 to 18 months,” says Eric Bosveld, senior advisor, food and agribusiness, for Denver investment bank SDR Ventures. The low-growth ag sector also repels some investors, who must endure a steep learning curve once they enter this space.

Farmers and companies servicing this industry, however, need money and guidance, especially if they want to scale. They increasingly welcome strategic buyers and investors attracted to an industry that soldiers on, even in bad economies. For sponsors willing to endure the challenges and pay their dues, the rewards can be fruitful.

“We’re looking at three to four investments in a calendar year in the space and haven’t seen any degradation in the number of opportunities,” says Jim Clark, a partner at PE firm Granite Creek Capital Partners in Chicago. Granite Creek has invested in upstream agriculture for more than 10 years.

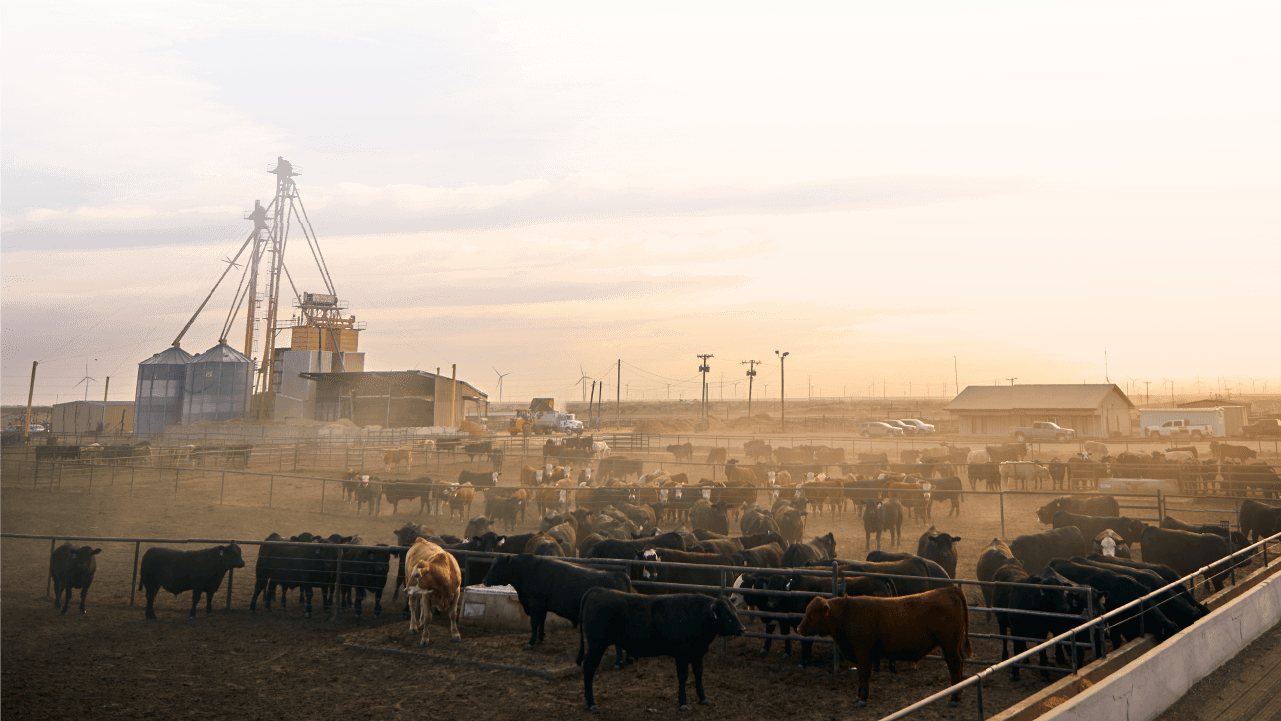

In 2024, the firm acquired Ritchie Industries, an Iowa maker of automated livestock watering products, and invested in Seedbox Solution, an Illinois-based provider of reusable packaging for the row crop seed industry, and Global Animal Products, an Amarillo, Texas, maker of trace minerals for farm animals. “We’re looking at companies that provide products or services to the farmer or rancher or livestock owner,” Clark says. “It’s a huge market opportunity for PE investing.”

Agriculture Advantages

Investors appreciate the diverse opportunities within agriculture from cattle ID and tracking to packaging and processing to technology that manages water or labor shortages.

“Anything that can make labor more efficient is really important, because the bodies aren’t there to do a lot of the work,” Mickelson says. Businesses that produce the same amount of supply more efficiently for a lower cost, rather than by adding more employees, are appealing, echoes Clark.

Tractor makers John Deere (NYSE: DE) and Kubota Corp. have acquired “companies that help with the shortage of water and shortage of people,” notes Boston-based agriculture and food consultant Peter Tasgal. In August, John Deere snagged GUSS Automation, an independent California maker of a semi-autonomous sprayer used in orchards, vineyards and bedded vegetable farms. One month earlier, St. Louis-based Azuria Water Solutions merged with Inframark, a Texas technology company that specializes in water and wastewater operations and maintenance. Azuria, backed by New Mountain Capital, provides technology to address aging water pipeline infrastructure. The company also announced four add-ons in 2025.

Controlled environment agriculture is also “a real area for growth because it’s not subject to the weather,” Tasgal says. “Eighty percent of your tomatoes are grown in greenhouses.” In August, salad maker organicgirl, backed by Arable Capital Partners, acquired Dole’s Fresh Vegetables division for $140 million. California-based organicgirl also bought Braga Fresh, a grower of conventional and organic vegetables, to augment Arable’s portfolio.

Challenges and Risks

These ag deals aside, 2025 was a lackluster year. In its recent Farm Sector Income Forecast report, the U.S. Department of Agriculture predicted that crop receipts would plummet in 2025, while animal and animal products receipts would rise significantly.

Some companies with positive cash flow attracted buyers, but other sellers refused to put their businesses up for sale due in part to the distress caused by President Trump’s tariffs, experts say.

“A lot of people are putting things on hold to focus on their internal operations or increase their valuations,” Bosveld says. “The general ag economy has to be in a position where growers are willing to take risks, and right now for the most part they are hunkering down, trying to stay afloat.”

Also, this conservative industry doesn’t often welcome change. For technology investors in the ag space, “Adoption is often a lot slower than what tech investors are used to, and that’s created some challenges,” Bosveld says. This puts pressure on agtech companies to create technologies that are “simple and easy to implement, with a clearly defined and measurable ROI,” he adds.

In addition, there is price volatility, flat commodity prices, rising input costs and inflationary pressures, notes Oakdale, Calif.-based Sean Haynes, an ag consultant and senior advisor for FOCUS Investment Banking. “At the crop production end it is low growth,” Haynes says. “Returns are very thin.” Investors need to understand “the breakeven point on crops” and the labor challenges before entering this space, he advises.

Bifurcated consumers also pose a challenge. High-end consumers keep shopping, while lower-income consumers won’t spend more for produce, Tasgal says. Growers often absorb these losses. And while PE investors love their five-year timelines, with a lucrative exit in sight, agriculture operates in its own bubble. “The margins are never going to be what they are for Nvidia (Nasdaq: NVDA)” he notes.

And agriculture, of course, sits at the mercy of Mother Nature. “The growing side is such a high-risk business,” states Orlando-based Michael Poole, managing director of PCE Investment Bankers, a middle-market advisor. “In Florida, if you own orange groves and then a freeze comes through, there go your groves. Because of the weather playing a role on the growing side, you need to hedge your bets.”

The Road Ahead

Most ag experts predict deal activity in 2026, though at a measured pace. Tasgal expects outdoor and indoor growers to merge, along with member-owned co-ops . “There is significant opportunity for further tech to be inputted into the ag world,” he adds. This can translate to M&A.

Additionally, says Haynes, “You’ll see a lot of activity focused on getting bargain purchases of distressed assets.”

Clark forecasts a status quo for his firm in 2026. “For the segment of the market we play in, and the number of transactions we’re pursuing, we expect it to be consistent,” he says.

Mickelson, however, remains optimistic. “There will be a lot of deals,” he predicts. “Demographically, the industry is not getting any younger, and when you have a down cycle and upcycle that is coming, both of those create opportunities to buy and sell businesses.”